Sweden Re was founded in 1914 and is the leading reinsurance corporation in the Nordic life and health insurance market with respect to both reinsurance and medical risk assessment. Since 2006, Sweden Re has been part of SCOR, one of the world’s largest reinsurance groups. With more than 2,000 employees and clients in over 80 countries, SCOR operates 39 offices around the world.

This article is a summary of the book; Larsson, Mats & Lönnborg, Mikael (2014). SCOR Sweden Re. 100 Years of Swedish (Re)Insurance History. Stockholm: Dialogos: that was presented in connection with the 100th anniversary of the company on the 11th of November 2014 (Larsson & Lönnborg 2014).

Introduction

The purpose of the reinsurance industry is to provide insurance for primary insurers. Primary insurers have fairly standardised policies, whereas those of reinsurers are often less so, more internationally oriented and likely to cover very large risks. There is little doubt that primary insurance policies, as well as an insurance market based on fixed premiums, would be difficult to sustain over the long run without reinsurance. Reinsurance enables portfolio diversification by the primary insurer in order to avoid the kinds of devastating losses that could threaten its survival (Kopf 1929; Golding 1930; Doherty & Smetters 2005; James et al. 2014; Borsheid & Haueter 2012).

Although Sweden Re was not the first reinsurance company to do business in Sweden, none of its predecessors survived for very long. Sweden Re was founded as a joint venture by a number of Swedish life insurers to handle their reinsurance requirements and limit their risks. The reinsurance business proceeded from the primary activities of the various insurance companies, as well as their need to minimize the associated risks. Insurance companies set a risk maximum, and any insured amount above the limit was redistributed to other companies. Thus, reinsurance allowed a company to accept extensive risks without jeopardising its survival (Palme 1923; Bergholm 1925; Englund 1940; Gerthewohl et al. 1980 & 1982; Elliot et al. 1995).

The general objective of Sweden Re has been to be the leading life reinsurance company, first in Sweden and since the 1990s, in the Nordic area. To reach that goal it has been of utmost importance to establish long-term and close relationships with its clients, primary insurance companies. This has only been possible through a high-level of competence, excellent market knowledge and understanding the needs and problems of direct insurers. It has been crucial to produce individual and customised solutions and concepts as well as explaining the content and providing them for clients. As a matter of fact, this is the essence of the company’s business and has been stated in a great number of annual reports, but according to the study by Larsson & Lönnborg (2014), it is very obvious that Sweden Re has managed just these measures. One of the most obvious pieces of evidence of this is that Sweden Re has survived for a century.

During the century that Sweden Re has existed, some major events and changes have been significant in forming the organisation and business of Sweden Re. In this article, we will address five events of special importance for making Sweden Re what it is today. The first event is the establishment of Sweden Re. The market conditions for reinsurance during the early twentieth century were propitious for creating a company with a specific task to spread the risks on the insurance market. However, this also had long-term implications well into the 1980s and led to a locked-in situation for the company.

The second event was consolidation of the insurance market between 1950 and the mid-1980s. This changed the ownership structure of Sweden Re but also transformed market conditions. Computerisation – the third event – was a response to larger volumes of transactions and lack of efficiency of Sweden Re’s administration. Increased efficiency meant larger profits for customers as well as for the company Sweden Re. The fourth occasion was the global challenge to the insurance market. It started in the 1970s but did not affect Sweden until the 1980s and 1990s (Larsson et al. 2005). This increased the pressure on Sweden Re’s business and made changes to the companies’ activities increasingly important. This development was closely connected to the fifth event, changes in ownership of Sweden Re.

The long-term development and the important changes in the market, business and development have been summarised in the companies’ own presentation of Sweden Re (Figure 1). This gives the picture of a company with a fairly stable market until the mid-1990s. But with changes in ownership, the possibility to generate profit from the companies’ business enhanced. The growing business volume was of course closely connected to the boom in the international market and possibilities to develop the Sweden Re’s business. A prerequisite for the development of Sweden Re – and the ability to embrace changes in the market – during the last century has been the stability of human capital and competence. Sweden Re has been a valued employer that attracted staff members to remain at the company for several years.

Figure 1

Figure 1

Source: Larsson & Lönnborg 2014, p. 209.

This was important in order to maintain and develop competence within the company. However, this could also become a problem if the competence did not match the changes in the market. One example of this was the computerisation of Sweden Re, which – after a decision by company management – was implemented by consultants and newly employed staff.

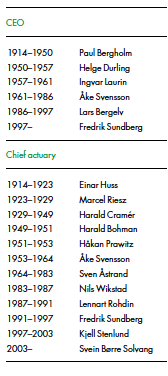

The leading positions in Sweden Re have already from the establishment been held by people with excellent knowledge about the insurance industry in general and actuarial issues in particular. Both CEO, and chief actuaries have been well-educated, sometimes with experience of academic research. In fact, actuarial competence has often been at the top level and the employees among the most wellknown mathematicians in Sweden. The CEOs of Sweden Re have always been people with actuarial competence, and most often with experience of other insurance activities, as well as from Sweden Re. Since Sweden Re was established, there have been only six CEOs, of whom the first, Paul Bergholm, stayed at this position for 36 years, see figure 2 (Larsson 1965). Even though the other CEOs have not remained at their positions for so long, the stability has been striking, which probably has helped to maintain and develop long-term relationship with clients.

Figure 2: Sweden Re’s CEO and chief actuary 1914-2014

When Eureko Re in the 1990s evaluated Sweden Re before a possible takeover, they also performed an overview of the staff of Sweden Re. One problem that Eureko noticed was that several members of Sweden Re’s management were over 50 years and that the limited staff could be a problem should one or several of them retire. However, this was only partly accurate. There were several years until retirement for parts of the staff and there were also younger employees with the necessary competence who were already employed at the company.

The staff of Sweden Re has on several occasions been the object of rationalisation. In the 1950s, when the turnover at Sweden Re did not develop satisfactorily, several employees left their positions, and the same thing happened during the 1980s and 1990s as an effect of rationalisation, computerisation, the loss of administration of the assets of Swedish Medical Association and changes in ownership structure. But even though the number of employees after World War II has fluctuated between 15 and 40, there has never been any striking problem in handling redundancies. Employees of Sweden Re, with their knowledge of risk evaluation and actuarial problems, have always been attractive in the Swedish insurance market. This is of course a tribute to the competence of the human capital of Sweden Re.

The establishment

Sweden Re was created as a means of cleaning up the life reinsurance market in Sweden and was to some extent an entrepreneurial venture, maybe not from a traditional point of view but nonetheless it was something new that emerged in collaboration. At the end of the nineteenth century and the beginning of the twentieth century, several life insurance companies were founded; however a large number of them were underfinanced and had problems surviving. One measure to finance the business was through accepting reinsurance treaties from foreign insurers that on the positive side generated a lot of income at an early stage. But the construction could be very costly in the long run and the companies could suffer severe losses. In the case of bankruptcies among small life insurance companies, this could jeopardise confidence in the entire market. In addition, it was regarded as important to limit the outflow of capital from Sweden through foreign reinsurance, and instead supply capital for the domestic industry (Bergholm 1925; Englund 1945; Englund 1993).

This started a discussion about founding a domestic life reinsurance company as a joint venture among Swedish insurers. Mainly two individuals discussed this issue, namely Filip Lundberg – the CEO of the industrial life insurer De Förenade, jointly owned by major insurance companies, – and Paul Bergholm – CEO of the minor life insurance company Brage that suffered partly from previously written reinsurance contracts. Through intensive negotiations with the managing directors of the leading life insurance companies at the time, it was possible to launch the idea of a life reinsurance company jointly owned by Swedish life insurance companies. Sweden Re became not only an instrument for sorting out the issue of reinsurance but an organisation that contributed to and facilitated collusion on the market.

The fact that CEO Paul Bergholm also became a member of the boards of the Swedish Association of Life Insurers and the Swedish Insurance Society (later on chairman) as well as editor-in-chief of the Scandinavian Insurance Quarterly also indicated that Sweden Re was part of the organised co-operation among Swedish insurers. The other initiator, Filip Lundberg, did only participate at the board of directors a couple of years in the early years of Sweden Re’s business. The reason was that he was CEO of the industrial life company De Förenade that only wrote so-called small insurances and didn’t practise any reinsurance. However, he returned to the board meetings in the 1930s when he became CEO of Victoria, even though he was formally not a member of the board. Filip Lundberg’s interest in creating a common organisation for life reinsurance was mainly to make sure to secure the legitimacy of the entire market (Grenholm & Cramér 1969).

Sweden Re was created to solve the immediate problems of the Swedish insurance market, but the long-term effects were considerable and influenced the reinsurance situation in Sweden for over 70 years. During these years, Sweden Re had a more or less monopoly position in the Swedish life reinsurance market. This gave stability, which is of the greatest importance for trust in both insurers and reinsurers. But this also distanced Sweden Re from developing new areas – which was not requested by the owners. And with voluntary and legal restrictions on profits and dividends, Sweden Re became more of a service organisation than a market-oriented company.

In the anniversary book of 1965 (p. 7), Tage Larsson summed up what had characterised Sweden Re during the first fifty years of business:

In fact, to a great extent the problems of [Sweden Re] have been less complicated than those of the most other companies, since the company is more concerned with mortality than with the value of money and interest rates, more with ideas than with mass work, and more with negotiating than with selling.

He continued by arguing that there were four main reasons that could explain why Sweden Re had become the central institution for life reinsurance in Sweden and an efficient ‘servant’ of life insurers.

First of all, the high propensity to co-operate – in spite of fierce competition – among the Swedish life insurers; otherwise a construction like Sweden Re would not be a possible solution for the market. Second, the high scientific standard of mathematicians, medical experts and risk assessors connected to Sweden Re. Third, the successful selection of CEOs of Sweden Re, which has been crucial in gaining legitimacy in the market. Fourth, the prominent technical methods developed by Sweden Re, in particular the idea of reinsurance on a risk premium basis.

Of course, the context of Sweden Re’s business has changed over time. No longer is the company solely a servant of Swedish life insurers, and nowadays the marketing aspects have become of more importance for the business. The ownership structure is of course totally changed, and that has made aspects of co-operation in the Swedish market obsolete. The market has been widened outside Sweden, mainly to Norway but also with minor engagements in Denmark and Finland. Still, the appointment of CEOs has been successful and managing directors have shown remarkable longevity, and developing innovative technical methods has continued to be at the heart of Sweden Re’s success formula.

Consolidation of the insurance market

Consolidation of the insurance market began shortly after World War II, when companies increased their co-operation within insurance groups, but at the same time working under their own name. This co-operation also opened the door to survival and development of cartelisation of Swedish insurance. However, when companies in the 1960s started to merge, the number of life insurers declined, as did the number of owners of Sweden Re.

During the following decades, three mergers of special importance for Sweden Re were completed. The first one in 1965 created the Skandia Group, which was a merger between all large joint-stock insurance companies (Englund 1982). The second merger in 1971 between a number of large mutual companies created the Trygg-Hansa Group, and the third merger in 1985 resulted in the Wasa Group. These three companies were, together with Folksam, the owners of Sweden Re in the late 1980s, with Skandia dominating the ownership with around half of the shares of Sweden Re. But with four large owners, the preconditions for keeping the ownership of Sweden Re together deteriorated (Larsson & Lönnborg 2007, 2009a & 2009b).

Especially the two largest groups, Skandia and Trygg-Hansa, started to develop their own solutions for reinsurance, and the need of, and interest in, keeping Sweden Re as a partner evaporated. The arrangement was finally broken when these companies decided to develop their own reinsurance companies and either sell their shares or close down Sweden Re. Folksam also left the partnership, which made Wasa the remaining owner of Sweden Re. When Wasa offered to buy the other companies’ shares the survival of Sweden Re was solved for the moment – as a subsidiary of Wasa International.

Thus, consolidation of the insurance market created the foundation for a new ownership construction of Sweden Re, and for the possibilities of developing the business of the company. However, the lack of capital and international contacts, as well as the fact that Sweden Re’s owner was a potential rival to all potential clients, hampered the development and Sweden Re stagnated during the new ownership, and it was not until the company was taken over by foreign owners that Sweden Re’s business started to develop faster.

Computerisation and efficiency

The computerisation of Swedish insurance began slowly in the 1950s. The principle of equity (fairness) was introduced in the insurance regulation of 1948 with the aim of cutting administrative costs for insurance and put pressure on insurance companies to rationalise their businesses. The first tests of computerisations were performed in the late 1950s and 1960s, but there was no general breakthrough. Computers and computer time was still a scarce commodity. But gradually the use of computers increased and the new technology would totally alter working conditions at Sweden Re.

Sweden Re was late in using computers and that is a bit surprising, since their index card registers were well-suited for computerisation. But when the use of information systems started to develop in the mid-1980s, it was very coherent and changed the entire business and administration. An advantage was that the systems were already adapted to each other from the start, which increased the efficiency of the computerisation process.

However, the largest advantage of the use of information systems was in handling databases. Especially the computer-based ru-register indicated the possibilities that could be won with a smoothly working system. With the development of a business-to-business system, it was possible for Sweden Re’s clients to have direct access to the information in Sweden Re’s databases. This did indeed put Sweden Re in the forefront of computerisation in the Swedish insurance market. The advantage of this system was even so great that Wasa’s non-life reinsurance company, with the help of people from Sweden Re, implemented a similar system. In the long run, this computerisation was absolutely necessary for the development of Sweden Re and the survival of the company after the changes in ownership in 1990.

The global challenge

Sweden Re had been created to solve life reinsurance for the majority of the Swedish life insurers. Together with substandard reinsurance, the reinsurance of ordinary life and disability insurance had built up the business of Sweden Re, and the market was still more or less the same in the 1980s. But with the deregulation of international financial and insurance markets, the possibilities to change the business and the challenges from the global market increased. Since Sweden Re’s clients had developed from Swedish companies to international business groups, the possibilities to find other reinsurance solutions had increased.

In order to survive this global challenge, Sweden Re had to be more adapted to international standards and traditions. Otherwise the risk for liquidation of Sweden Re would be an immediate alternative – as has happened with fellow subsidiaries in the Nordic countries. The consolidation of the reinsurance market to fewer companies was an international phenomenon that was based on deregulation of international markets and the flow of global capital between countries. These larger reinsurance companies with extensive capital assets could undertake larger business agreements and reduce risks for their clients.

After the deregulation of the Swedish financial and insurance markets, institutional preconditions also favoured an international development for Sweden Re. However, the problems were – as already mentioned – the lack of capital and international inexperience. Connected with this was also the strong tradition of the Swedish insurance model with remnants of the strong Swedish regulatory tradition. Taking this into consideration, it might be surprising that Sweden Re managed to survive and develop.

International owners and market development

The Swedish insurance market has experienced revolutionary changes over the last 25 years. Several large Swedish joint-stock insurers have been transformed and ownership changed. For instance, Trygg-Hansa merged with the Swedish bank

SEB in 1997; the life insurance operations were kept but the non-life portfolio was sold to Danish Codan (in turn owned by British RSA). In addition, Skandia separated and later sold its non-life portfolio. Furthermore, the remainder of Skandia was taken over by Old Mutual in South Africa, but the Swedish part of the group was later purchased by the subsidiary Skandia Life and transformed into a mutual insurance company. In addition, due to the financial crisis of the 1990s, the lack of capital and losses on international insurance, every Swedish insurance company withdraw from international business and instead focused on the domestic market (Larsson & Lönnborg 2010 & forthcoming).

In the 1990s, Wasa International suffered major losses, and in order to make the company competitive in the international market, it was necessary to have a major infusion of capital. Considering the financial crisis at the time, it was difficult to obtain resources from the capital market, and in the end, the decision was to withdraw from the international market and put the business in run-off. This in turn made the ownership of Sweden Re questionable and Wasa started to look for a buyer of all or parts of the company.

The first option was Eureko Re, but after a due diligence process demonstrating that Sweden Re was too dependent on business generated from Wasa, this transaction failed. The second and realised transaction in 1995 was with the German Gerling Group, and the problem of being too closely connected to Wasa was solved through a co-operation agreement, where Wasa promised to remain a minority owner for a five-year period. In short, the new ownership structure of Sweden Re was a blessing in disguise for the company. Sweden Re was transformed into a competitive reinsurance company with higher shares of reinsurance premium kept for own account, and the entire business was restructured. Being part of an international financial group – and changing its name – also meant access to international capital.

The change of Sweden Re can be illustrated by the fact that for the first time ever in the company’s history a marketing department was constructed within the company. To return to the quote by Tage Larsson in the 1960 s, now Sweden Re started to focus not only on negotiations but also on selling. In spite of the financial turmoil at the Gerling Group and the transformation into the company Revios, Sweden Re showed an outstanding performance. Uncertainty about the future of Revios and the group was finally solved through a takeover by SCOR in 2006. Again, Sweden Re became part of an international financial group, and today the SCOR Group is the fifth largest reinsurance company in the world.

Sweden Re has managed to adapt to changing ownership structures which has resulted in a reorganisation to cope with a wider compliance scheme, improved routines and increased reporting demands, which is a natural consequence of being part of an international group noted on several stock exchanges. The last major change is that Sweden Re, instead of being a subsidiary, became a branch of SCOR in 2013. This can hopefully make it easier for Sweden Re to cope with financial constraints but also contribute to generating new business in the future.

To sum up, it has been crucial for Sweden Re to be part of a viable international financial group to make the company a competitive player in the life reinsurance market. This would have been possible with a Swedish owner with a large international portfolio, but considering that every Swedish insurance company had withdrawn from international business, this was in practice impossible. Therefore, we can state that without foreign owners – Gerling, Revios and finally SCOR – Sweden Re would most likely have been eliminated from the market and never been able to survive for a century.

This is only a brief sketch of SCOR Sweden Re’s first century in business, and the entire story of the company’s history is available in Larsson & Lönnborg (2014).

References

Bergholm, P. (1925), Återförsäkringsaktiebolaget Sverige 1914 11/11 1924. Några anteckningar rörande bolagets tillkomst och utveckling. Stockholm: Återförsäkringsaktiebolaget Sverige.

Borscheid, P. & Haueter, N. V. (2012). World Insurance. The Evolution of a Global Risk Network. Oxford: Oxford University Press.

Doherty, N. & Smetters, K. (2005). ’Moral hazard in reinsurance markets’. Journal of Risk and Insurance. 72(3).

Elliot, M. V., Webb, B. L., Anderson, H. N. & Kensicki, S. R. (1995). Principles of Reinsurance. Volume 1, 2nd edition. Pennsylvania: Insurance Institute of America.

Englund, K. (1940). Återförsäkringsaktiebolaget Sverige 1914-1939. Redogörelse för bolagets verksamhet under de tjugofem första åren. Stockholm: Ivar Haeggströms.

Englund, K. (1945). Märkesmän inom svenskt försäkringsväsen. Biografiska snabbteckningar. Stockholm: Gjallarhornet.

Englund. K. (1982). Insurance companies on the move: From Skandia to the Skandia group, 1855-1980. Stockholm: Skandia.

Englund, K. (1993). Skandiamän och andra försäkringsmän 1855-1970. Femtio biografiska studier. Stockholm: Skandia.

Garethewohl, K. (1980 & 1982). Reinsurance. Principles and Practice. Vol. 1 & 2. Karlsruh : Versicherungswirtschaft.

Grenholm, Å. & Cramér, C. (1969). Filip Lundberg. Förgrundsman i svensk livförsäkring. Stockholm: Svenska Livförsäkringsbolags Förening.

Golding (1930). A history of reinsurance with sidelights on insurance. Offered as a memento of fifty years' service in the reinsurance world by Sterling offices limited. London: Sterling.

James, H., Borscheid, P., Gugerli, D. & Straumann, T. (2014) (eds.). The Value of Risk. Swiss Re and the History of Reinsurance. Oxford: Oxford University Press.

Kopf, E. W. (1929). ’The Origin and Development of Reinsurance.’ Proceedings of the Casualty Actuarial Society (Casualty Actuarial Society) XVI.

Larsson, M., Lönnborg, M. and Svärd, S-E. (2005), Den svenska försäkringsmodellens uppgång och fall. Stockholm: Svenska Försäkringsföreningens Förlag

Larsson, M. and Lönnborg, M. (2007). ’Ömsesidig försäkringsverksamhet och den svenska försäkringsmodellen’, Scandinavian Insurance Quarterly, No. 1, pp. 85-100.

Larsson, M. and Lönnborg, M. (2009a), ’Den svenska finansmarknaden i ett långsiktigt perspektiv’. in: Grip, G. (ed.). Folksam 1908-2008. Mer än endast försäkring, volym 2. Stockholm: Informationsförlaget: pp. 210-255.

Larsson, M. and Lönnborg, M. (2009b). ’Samverkan och konkurrens inom svensk försäkring’. in: Grip, G. (ed.). Folksam 1908-2008. Mer än endast försäkring, volym 2. Stockholm: Informationsförlaget: pp. 179-209.

Larsson, M. and Lönnborg, M. (2010). ‘The History of Insurance Companies in Sweden: 1855-2005’, in: Caruana de las Cagigas, L. (ed.). Encuentro Internacional sobre la Historia del Seguro. Madrid: Fundació Mapfre: pp. 197-237.

Larsson, M. & Lönnborg, M. (2014). SCOR Sweden Re. 100 Years of Swedish (Re)Insurance History. Stockholm: Dialogos.

Larsson, M. & Lönnborg, M. (forthcoming). ‘The Survival and Success of Swedish Mutual Insurers’. in: Pearson, R. & Yoneyama, T. (eds.). Corporate Forms and Organisational Choice in International Insurance. Oxford: Oxford University Press.

Larsson, T. (1965). ’The men, ideas and activities’. In: Sweden Reinsurance Company 1914-1964. Stockholm: Återförsäkringsaktiebolaget Sverige.

Palme, S. (1923). Thule under 50 år. Stockholm: Hæggström.