It’s been two years since McKinsey wrote about personalization as the future of life insurance. Yet for many, buying and owning a policy today doesn’t feel radically different than it did 2 or even 20 years ago. While insurers, reinsurers, distributors, and policyholders can all agree that greater personalization is necessary, the challenge is how to make that happen while still providing comprehensive coverage at an affordable price. At least part of the answer lies in engaging with customers on H&W.

Due to the proliferation of health apps and wearables, consumers have more data about their health and lifestyle than ever before – and they’re often willing to share their data if they see the value in doing so. Swiss Re’s “Global COVID-19 Consumer Survey 2022” found that globally, two thirds of consumers are open to sharing personal data or health results in return for a benefit (e.g., personalized health advice, faster application process, discounts). In advanced markets, such as North America, survey respondents were primarily attracted to H&W apps that 1) help them improve their health and 2) help them understand their current health status. Our survey also revealed that while price is the most important factor in insurance buying decisions, the inclusion of additional services is also a key consideration, particularly in the US market.

Engaging with customers on H&W has strong potential to produce shared value for all parties involved:

• Consumers can purchase more relevant products at the right price point, experience improved health and longevity, and may qualify for meaningful financial incentives and rewards as a result.

• Distribution experiences sales growth and can tap into potentially infinite touch points with their customers as life changes.

• Insurers and reinsurers build customer relationships that go beyond a policy in a drawer and an annual bill – resulting in better mortality and persistency and maximizing the lifetime customer value.

• Society as a whole benefits when people are healthier and better protected financially.

Many insurers recognize the opportunities that H&W engagement may create, but some struggle to quantify the impact and make the case for launching a H&W engagement program. Our experts believe, when structured appropriately, H&W engagement programs can help policyholders improve their wellbeing, strengthen their loyalty, and bring longterm commercial benefits to insurers (e.g., improved mortality and persistency and sales growth).

This paper focuses on the commercial benefits of engaging with customers on H&W with the aim of helping innovative insurers:

1) Make the case that H&W engagement programs can improve mortality and persistency and have a positive ROI, and

2) Measure and maximize the impact of their H&W engagement program.

H&W engagement programs can improve your bottom line

Based on our global research and experience working with carriers on H&W engagement programs, we have developed a model to assess the business impact of implementing a H&W engagement program depending on a variety of key assumptions. Our modeling shows that it is possible for insurers to run commercially viable H&W engagement programs that improve mortality and persistency and have a positive ROI.

Potential Mortality & Persistency Improvements

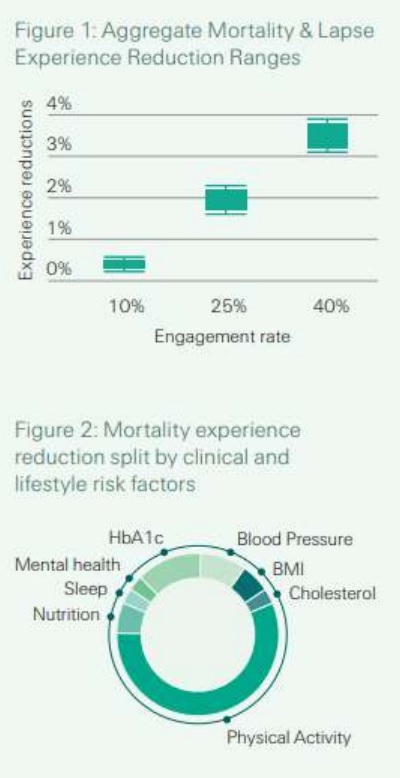

If a US insurer initiates a H&W engagement program on a fully underwritten term mortality product and engages 40% of policyholders on an ongoing basis, our model estimates an aggregate mortality and lapse experience reduction of up to 3.8% across the entire book of business. For programs with a 25% engagement rate, we estimate an aggregate mortality and lapse experience reduction of up to 2.2% across the entire book of business (Figure

1)[1].When breaking this down by the relative impacts due to positive persistency, positive initial selection and ongoing positive behavior change, we see that more than half of the overall benefit comes from true behavior change – policyholders making better lifestyle choices and therefore leading longer, healthier lives. This is an important consideration for carriers who might already have great persistency and question the incremental value of engaging with policyholders on H&W.

When looking at the relative impact from various clinical and lifestyle risk factors, physical activity is the main driver of improved mortality (Figure 2). This makes sense for a few reasons:

• There’s a strong link between physical activity and reduced mortality.

• It’s relatively easy for people to modify physical activity levels.

• H&W programs tend to monitor and incentivize physical activity.

While the impact of some risk factors may look small, when considering the aggregate impact across an entire book of business, even slight improvements to mortality and persistency for a given risk factor may translate to meaningful cost-savings for insurers. Additionally, the mortality and persistency improvements will be more profound for certain segments of the population (e.g., highly engaged policyholders with below average health or policyholders above age 50).

![]()

Potential Return on Investment

Based on our analysis of the costs and benefits of launching and running a H&W engagement program, a successful program with a 25% engagement rate can be ROI positive. And, with 40% engagement, profitability may increase by up to 9% compared to not having a H&W engagement program. This analysis includes the expenses associated with policyholder rewards and premium discounts, the platform implementation and user licensing fees, and the additional resources needed to launch and run the program. It also factors in the expected improvements to mortality and persistency but does not consider added benefits from increased policy sales, upselling and cross-selling, which may further increase profitability and ROI.

How to maximize the impact of your H&W engagement program

For insurers looking to maximize the commercial viability of their H&W engagement program, we recommend focusing your efforts in three key areas:

1. Maximize H&W program take-up & engagement rates

As we pointed out previously, improvements to mortality and persistency are driven by the ability to attract and retain healthier lives, and the ability to help people overall live healthier and longer lives. This means that if you’re looking to maximize the impact of your program, take-up rates and engagement rates matter. For example, as illustrated in Figure 1, improving engagement from 10% to 40% increases the aggregate mortality and lapse experience reduction more than seven-fold (from .5% to 3.8%).

Successful H&W engagement programs will have a clear target audience, an effective strategy for reaching the target audience, and a unique and compelling design to keep people coming back day after day, year after year. If you get this right, seemingly high takeup and engagement rates are achievable.

Here are some questions our clients have found helpful to think through:

• Who are your target customers – New or existing policyholders? People with certain chronic conditions or people who are already healthy and active?

• How will you reach your target customers?

• If you’re targeting in-force policyholders, do you have their current contact information (including email address), and what would make them more likely to open a message from you?

• Will everyone automatically have access to the program, or will people have to optin?

• Can your distributors clearly articulate the benefits of the program to new potential customers and tell them what to expect when signing up?

• Does your program design include relevant goals and challenges and provide the opportunity for policyholders to connect with family or a wider community of users?

• Are your incentives and rewards compelling?

2. Help policyholders sustain meaningful behavior changes

In addition to acquiring, onboarding, and engaging customers, to maximize the impact of your program, you’ll have to think about how to help policyholders lead longer, healthier lives. Encouraging people to substitute one action for another is hard. Supporting them to adopt healthy long-term habits and lifestyles is even harder. But luckily, it’s not impossible!

Our research has shown that successful H&W engagement programs focus on helping policyholders improve across a mix of clinical and lifestyle risk factors. In general, clinical risk factors (e.g., BMI, blood pressure, HbA1c, and cholesterol) are more traditional and reliable indicators of overall health, but lifestyle risk factors (e.g., physical activity, nutrition, mental health, and sleep) are easier to monitor, incentivize, and improve. Focusing your efforts on helping policyholders make small, but ongoing lifestyle changes can positively impact biometric values, clinical outcomes, and your overall mortality experience.

Figure 2 showed that physical activity was one of the main factors driving mortality experience reduction in our analysis of H&W engagement programs, but this does not mean that your program should ignore the other clinical and lifestyle factors. Particularly if your target customers include people with impairments, it might make sense to focus your efforts on another risk factor. For example, a program intended to help diabetics or prediabetics could focus on HbA1c and incentivize behavior changes to positively impact that risk factor. Although diabetics may be a smaller segment of an average insurance book, people who are in a poorer state of health often have a larger potential for meaningful behavior change. Diabetics who engage and improve their HbA1c to pre-diabetic levels may substantially reduce their mortality risk, resulting in a strong impact on the overall success of the H&W program.

3. Use H&W engagement to grow with new & existing customers

Consumers are increasingly seeking and selectively choosing products better aligned with their needs, which means innovative and personalized products will continue to gain traction in our market.

For insurers looking to maximize the impact of their program, it’s important to consider the big picture - what’s possible with a H&W engagement program? We’re seeing that in addition to positively impacting mortality and persistency, H&W engagement programs can contribute to top line sales growth and increase customer lifetime value.

Consider the benefits of regularly collecting policyholder clinical and lifestyle data. With ongoing data collection, it’s possible to periodically reassess a policyholder’s risk and provide dynamic pricing adjustments or increase the coverage amount to reflect improved health and longevity. For healthy customers, this could be a fun perk or extra incentive from their insurance company. For others, this could be an important tool that helps bring the cost of life insurance within reach. Ultimately, insurers can use the rich and continuous stream of data to offer the right product, at the right price, at the right time, which is exactly how companies will thrive as the life insurance industry continuously evolves.

For many insurers, taking full advantage of H&W engagement in this way may require a broader cultural shift – one that embraces the concept of shared value and moves the organization from transactional to lifelong relationships with customers. While it can be hard to quantify the ROI of such a shift, the potential benefits (e.g., improved brand image, wider customer reach, upsell and cross-sell efficiencies) indicate that it could be well

[1] This analysis is based on our global experience of a fully underwritten 20-year term mortality product without preferred stratification. We assume that the product receives strong acceptance in the market, the program has been in operation for 2+ years, 70% of policyholders elect to participate in the program, fitness assessments are run annually, and policyholders' lifestyle risk factors are tracked regularly (at least weekly or monthly).